PART 1

PART 2

PART 3

PART 4

PART 5

PART 6

Monday, December 27, 2010

Thursday, December 23, 2010

What IHS predicts for global economy in 2011

I said I wouldn't post this year anymore but I received an interesting report today so I decided to share with you. This report is from International Business Times.

What IHS predicts for global economy in 2011

By IB Times

Contrary to the prevailing view, the U.S. economy will gain growth momentum in the year ahead, while GDP will grow stronger in Europe and Japan, research firm IHS Global Insight has said in its forecast for 2011. The report, written by IHS Chief Economist Nariman Behravesh and IHS Global Insight Economist Sara Johnson, also says that though emerging markets growth will slow down, their growth will still be three times faster than that of the developed world.

The following are the main forecasts by IHS:

More stimulus will push unemployment below 9 pct in US

The U.S. recovery will pick up steam as the year progresses. In 2011, the U.S. economy is likely to be firing on more cylinders. Housing investment will begin to recover and the United States will enjoy export-led growth. Additional fiscal stimulus will add 0.6 percent to growth in 2011 and push the unemployment rate below 9 percent by year's end.

Europe, Japan growth to be stronger

Europe and Japan will also see slightly stronger GDP growth in the second half of 2011. The pace of growth in Europe is slowing, mostly because of fiscal tightening and jitters about sovereign debt. Stronger exports and improved consumer spending (especially in Germany) will help by mid-year.

China, Brazil growth will diminish markedly

Emerging markets will slow, but continue to grow three times faster than the developed world. Among the big emerging markets, China and Brazil will see the most pronounced slowing trends (as fiscal and monetary tightening is used to cool these economies), while growth in India and Russia will not suffer much (if at all).

Rates will stay unchanged in G-7, rise in BRICs

Interest rates will remain on hold in the G-7, but keep rising in the BRICs. The Federal Reserve, European Central Bank, Bank of England, and Bank of Japan are all going to keep policy rates on hold through most of 2011. In contrast, central banks in many of the large emerging markets and a few developed countries (e.g., Australia and Norway) will likely continue raising interest rates in 2011.

European economies will go for more fiscal tightening

Fiscal policy will become tighter in many large economies. Most countries in Europe will be tightening fiscal policy—some of their own accord and some under duress (e.g., Greece, Ireland, Portugal, and Spain).

Commodities' rollercoaster ride to go on

Commodity prices will move up gradually. The rollercoaster ride of commodity prices could continue. By the end of 2011, most commodity prices will be 5–10% higher than today. Factors other than demand growth (e.g., inventories, excess capacity, exchange rates, and speculative activity) will influence the extent of increases.

Inflation to remain inconsequential in developed economies

Inflation will not be a problem in the developed economies, but will rise in many emerging markets. Consumer price inflation in the advanced economies will average around 1.4% in 2011, compared with 5.5% in the developing world. Strong growth and fixed or managed exchange rates will contribute to upward price pressures.

Trade imbalances to stay the course

Global imbalances will neither worsen nor improve by much. The U.S. current-account deficit is likely to stabilize around $500 billion. A weaker dollar and strong emerging markets’ growth will help exports, but rising oil prices will raise import costs. Current-account surpluses of China and the Eurozone will hold steady for awhile.

Dollar will rise

The dollar will slide against most currencies, with the possible exception of the euro. A two-speed world and still-large global imbalances will have a predictable impact on exchange rates—downward pressure for the ―"crawling" economy currencies and upward pressures for the ―"galloping"economy currencies.

Wednesday, December 22, 2010

Last post of the year

Today I was thinking about something to write in here but I didn't have anything in mind so I decided to write the last post of the year so I will be able to take a time for me and allowing me to be able to start a new year with fresh, smart and more advanced ideas.

If I'd be able to define this year with one word it would be initiative due to the voluntary work as a teacher, the initiative to live just by myself, the initiative to create this blog and the initiative to study to take the certificate CPA-20, those would be some of the things that I did to try to turn myself a better person. Although I didn't get an internship as I'd like to, I'm with the kinda feeling that I gave the best of myself during the tasks I had to do and that's why I believe that future still hold a nice story to me.

I want to thank for all the visitors on this blog. I got excited when I receive about 300 page views on just one week when I started to write in here.

I would like to wish for all of you (known and unknown) a very nice Christmas and a faboulous 2011 full of success.

This is the wishes from a dreamer but a daring person!

See you in 2011.

Wednesday, December 8, 2010

Treasury bond prices sank for the second day on Wednesday

Teasury bond prices sank for the second day on Wednesday due to the deal to extend tax cuts enacted during George W. Bush presidency, according to Reuters. I wrote on August 23 on 'Increase on capital taxation for 2011' that in 2011 those benefits of tax cuts would expire because the american debt should climb to 13,7 billion dollar or 65% of GDP in the end of 2010. So, raising tax would control that deficit. But the current economic scenario says that is better to keep the tax cuts to generate a stimulus to the economic growth but can increase a fear of inflation, affecting directly on teasury bonds because the market believes that it can mean an increase in interest rates. So today the dollar rose againt a basket major currencies due to that perceptions about the american economy and pushing up the gold price. You can see on the chart below that investors are running to conservative assets such as gold and the price of 10 year bond interest rate is moderately getting higer because investors require more return in that kind of asset.

Wednesday, December 1, 2010

Debt crisis around European Countries

Today I was reading a market signals sovereign risk report released by Moody's. The report related that Portugal and Spain default probabilities had climb to a record as Ireland's bailout failed to mollify the capital market. So, I thought that would be interesting to cut and copy a graph from that report:

According to Moody's, CDS-Implied EDF measures use CDS spreads to accurately determine an entity's default risk. You can find out more at the website.

According to Moody's, CDS-Implied EDF measures use CDS spreads to accurately determine an entity's default risk. You can find out more at the website.

What we do in life (present) echoes in eternity (future)

This is the first time I post something related to my personal interests. I'm starting this post with this music because now I can enjoy myself a little bit (I'm on vacation). Here is a big, magnificent, splendid work from Antonín Leopold Dvořák that I appreciate a lot. It's a combination of energy and calmness at the same time as we hear the movements and by the way, I listen to this concert almost everyday!

However, this is just a plus. The main subject of this post is related to a meeting I had with the course director to talk about the classes and the progress of the course because I'm the class representative of my class.

At that time, students were complaining about early readings for class that the teacher was demanding. They believed that it was not necessary and that the teacher should not force that kind of reading. So he started to ask questions during the class about the previous readings and nobody was able to answer it and consequently asking them to leave the class.

As a class representative, I told the problem to the director and he very was skeptical about it, I could see his face expressing anger and intolerance. He told me that the readings were part of the learning agreement we signed when we enter college and he drew on the blackboard a graph explaining how important is to keep reading and what were the probabilites to success following that step. That graph was derived from a study which I forgot the authors but that graph I would never forget so I would like to share this with you:

He told me that people will just be able to be on the top of a big organization if they study a lot to develop their conceptual skills. Those positions require a lot of reading to be able to have an eficient discussion, follow tendencies and think strategically. He also said that at that time we will responsible to give the gidelines to the company's future, that's why the directors need a lot ot conceptual skills.

At the end of the meeting he gave me an advice: "Marcel, try to pass that message to your class and don't worry about the results. We can distingish early on who will or won't succeed."

Monday, November 22, 2010

"Money lost, nothing lost; Health lost, much lost; Character lost, everything lost."

Lately I’ve been writing about economics and finance that are subjects I really like but don’t reflect my interests. Today when I was watching the Bloomberg TV where 3 Hedge Funds were being raided by FBI due to insider trading, the reporter asked to the interviewee: “What are the consequences for the ordinary traders?” Then the interviewee said: “You know, this shakes the market structures. You buy a stock because you trust in that company. When a case of insider trading happens, how can people trust in each other?” and that’s when I thought: “I must need to write about it, character has always been a good interest for me.

Everyone knows that monetary relationships are based on trust, it means we are in a fiduciary system so a prerequisite to get a job would be to demonstrate confidence, character and responsibility above all the technical skills. However nowadays people are hired and paid due to their achievements, technical skills and academic education, this is so wrong I think. I’ve been on some group internship interview and I haven’t heard of anyone saying about character or something like that, they disguise personality through their perfectionist speeches to be hired. Well, there is a need to have a little bit of malice but we can’t let this be the main selection item.

To own a character is something very complicated nowadays when there are a lot of easy ways to achieve a goal in a short space of time, this can be magnificent, but there is no lie sustained for a long period of time. I believe time make us see the difference between bad and good. Time is, no doubt, the god of truth; it is the main responsible for the downgrade of empires owned by bad faith; and guarantee the wealth and stability for those whom were responsible and did their homework. Once I read a certain Chinese proverb that said a lot of thing about breach of trust: "Money lost, nothing lost; Health lost, much lost; Character lost, everything lost.

So I think people should valorize a little bit more the people character, find out if they are truthful and responsible. When I own my Investment Bank I’ll assure to interview any candidate that tries to get a job and work for me and with me. We cannot depreciate the personal relationships based on honesty because it is this relationship that paves the way to a better future."

Sunday, November 21, 2010

Brazil’s Tax on Capital Inflows, 2009–10

Today I was reading the Global Financial Stability Report released by IMF and I saw a very nice text about the brazil's tax on capital inflows. It is so interesting to read about it because I believe many countries such as Indonesia or Thailand will adopt this measure to slow down the capital inflow on their countries to avoid bubbles on assets.

"Brazil’s reimposition of an upfront tax on capital inflows in October 2009 triggered a wave of interest in many countries in the potential use of such measures to limit exchange rate appreciation. There is evidence that the Brazilian measures worked to change the composition of capital inflows and that they had a small but discernible impact on interest rate arbitrage.

However, they do not appear to have reduced aggregate capital flows into Brazil. In response to heavy portfolio inflows and substantial exchange rate appreciation during the preceding seven months, Brazil imposed a 2 percent entry tax (the IOF) on inflows to domestic bond and equity markets on October 19, 2009.1 Other types of capital flows, including direct investment, and dollar borrowing by Brazilian banks and firms, were not directly affected. The Finance Ministry announced that the measure was intended to combat speculation in capital markets, and to counteract the appreciation of the real, which it viewed as damaging export industries and employment. This was not the first time Brazil had employed controls on portfolio inflows—up until October 2008 it had levied a 1½ percent tax on bond (but not equity) inflows, but the authorities had eliminated the tax in response to the financial crisis.

Nominal appreciation against the dollar came to an end after the IOF was imposed, but reserves continued to rise steadily and the real continued to appreciate against the euro. Daily exchange-rate volatility was essentially unchanged after the tax. Foreign reserves continued to accumulate but at a reduced pace of about $100 million a day, compared with a little more than $200 million a day in the seven months before the tax was imposed. Chow breakpoint tests fail to show a decisive structural break associated with the tax for either reserves accumulation or for the dollar exchange rate. Foreign investors appear to have exploited some opportunities to divert flows away from investments on which the IOF would have a significant impact to those where it would not. Equity flows, which had reached a record pace in March-October 2009, and for which the effects of the IOF would have been significant, did diminish after October. However, and somewhat surprisingly, the rate of inflows into domestic bonds, where the impact of the IOF should also have been large, remained quite robust after the IOF was imposed. There were increases in short- and long-term dollar borrowing, neither of which is subject to the IOF in its present form. Foreign net long real positions in the domestic derivatives market, for which the effective incidence of the tax would be much lower than in the bond market, have also increased on average since the IOF. Futures-implied offshore interest rates can be constructed and compared with actual interest rates to test the effectiveness of arbitrage under the capital inflow tax. The nondeliverable-forwards (NDF) implied interest rate in Brazilian reais, based on the offshore nondeliverable currency forward, f90,off , can be calculated as:

iBRL,off = (1 + is) (f90,off |e)4 – 1.

This measure can then be compared to the onshore Brazilian three-month interest rate to determine a “basis spread,” as BSoff = (iBRL,off – iBRL). Full covered interest parity would entail that this be zero. For most emerging markets, however, basis spreads are not zero, even under normal market conditions. If the IOF is effective in breaking the link between domestic and foreign fixed-income markets, or in inserting a wedge between the two, this should be evident in market prices. If the new regulations eliminate arbitrage, or impose a cost of arbitrage between domestic and offshore markets, then there should be a difference between the implied interest rate in Brazilian reais available offshore through the NDF market, and the interest rate in reais available onshore in Brazil. The implied interest rate in reais should be lower offshore, where the IOF cannot be collected.

The basis spread derived from NDF trading should become negative, entailing a lower-than-market interest rate in Brazilian reais. If the 2 percent IOF is fully binding and if there had been full arbitrage before it was imposed, then the basis spread should widen by 2 percent on instruments with a one-year maturity. In the event, offshore basis spreads showed small but discernible signs of shifting in the period after imposition of the IOF. Offshore NDFs strength- ened relative to onshore currency forwards, and the NDF-implied basis spread did widen, although by only a fraction of the 2 percent (or 8 percent for 90-day instruments) that would occur if the IOF were fully binding. Both of these relative movements of offshore spreads were in a direction and of a magnitude consistent with a small but discernible effec t of the tax on cross-border arbitrage. There was little movement in onshore spreads. Overall, movementsin Brazilian basis spreads did not diverge appreciably from those of comparable emerging economies that took no special actions during this period, suggesting that the net impact of the IOF on interest rate arbitrage was not large." - IMF World Economic Outlook, October 2010.

Thursday, November 11, 2010

Exemplo de Carteira usando conceitos de Harry Markowitz

Read this post in english - click here.

Read this post in english - click here.Sempre quando procurei na internet nunca achei exemplos práticos que ajudassem o melhor entendimento sobre o que Markowitz apresentou em seu modelo de Portfólio. Deste modo, coloco a disposição um exemplo de carteira composta por 5 ações e seus respectivos retornos, riscos e porcentagem investida em um Portfólio. Qualquer duvida que surgir, poste seu comentário abaixo que estarei a disposição para ajudar.

Baixe aqui o exemplo em excel de Portfólio seguindo os conceitos de Markowitz.

Monday, November 8, 2010

Brazilian Stock Market Responding to Capital Inflows

Brazil and other emerging economies are experencing a resurge on capital inflows. There are two opposite consequences, on the one hand, the capital inflow have provided a boost on domestic demand, but on the other hand, these flows have increased concern about domestic overheating, external competitiveness (currency apreciation) and hightened risks of a potencial booom-bust cycle. There capital inflows have induced booms in many equity market, and concerns about asset price bubbles have been growing, according to the World Economic Outlook released by IMF.

In Brazil it is possible to see this boom caused by the foreign investors on the derivatives market (Figure 1) and stock market (Figure 2).

Figure 1. 1 Year BM&F Flux

Figure 2. 1Year IBovespa Flux

Saturday, November 6, 2010

Chronic problems of economic order

At first, headlines as this one looks like a little bit abstract for us, but these problems are things that we should have in mind, we should know how to discuss it and have a critical look at it. Have you ever thought about if you had to pay almost a 100% of your incomes to the State and in return don’t receive a good Medicare, social care or Medicaid? That’s what I’ll talk about in this post and by the way, I suggest two interesting contents: : I.O.U.S.A (Movie) and the book: Empire of Debt by Bill Bonner and Addisom Wiggin .

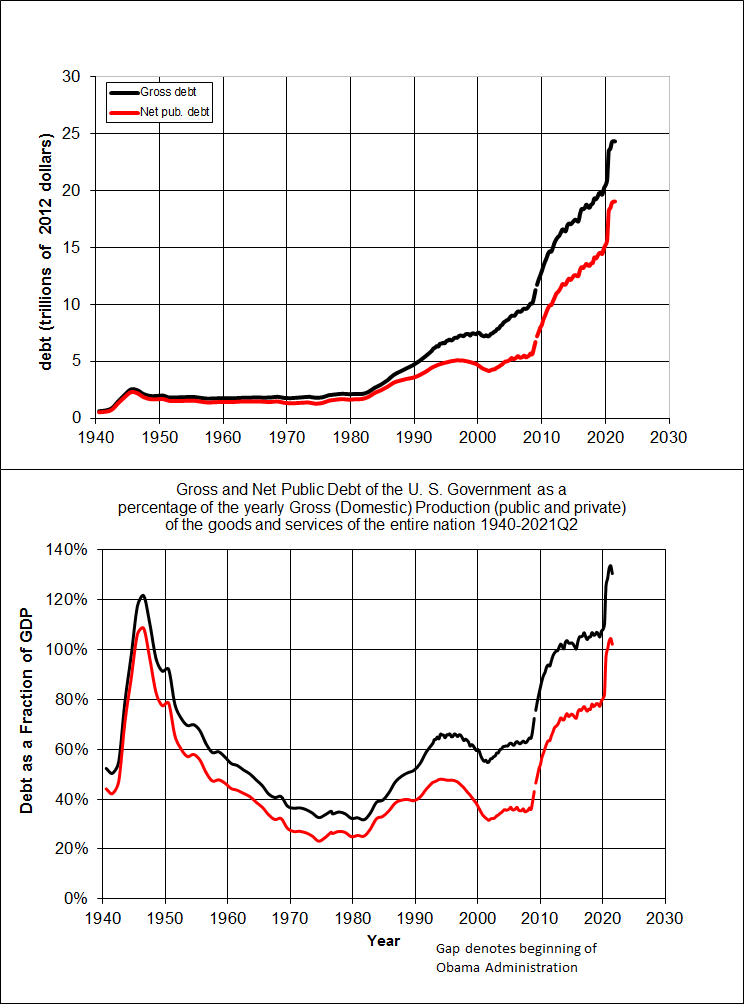

I begin this post with an interactive chart from Financial Times, click here to see the chart. We can see that public or federal debt in US in 2007 was around 42% of GDP and can hit 85.5% in 2015. Do you think this is comfortable? In 2007, the Japanese federal debt was around 81.5% of the GDP and can reach in 2015 the mark of 154.7 % of the GDP.

The federal debt occurs when the outcomes are bigger than the incomes and we express that result as a percentage of the GDP. The increasing or decreasing in this number depends on the monetary policy the country is using; it can be a contractionary, expansionary or neutral policy. People say that public deficit is used to stimulate the economy so in the future the country can enjoy that result. But, are we prepared to that supposed future? Take a look at the U.S gross and public debt chart. Do you think that this is healthy?

Now, take a look at it :

The Greece debt is more than 100% of the GDP. That's not healthy and that's why the government is heading for austerity measures. France government is doing that too, the country is set to raise the national retirement age in a bid to overhaul the nation’s government-run pension system and restore its ailing public finances, according to European Institute.

The most dangerous problem is realated to the ageing of the world population because this can represent a potencial meltdown of any nation.

Why this can mean a meltdown for any nation? Just take a look at that picture above and you will going to see for yourself. As the population get older, the government will colect less and will have to pay more for those people who contributed for the previdence all their life. More retirees means more spent with healthcare, how the governments will pay for it if he will receive less than before? Don't you agree that people can have less quality of life? Don't you think the government will rise taxes to equalize the bill? Today, most of government in the world are having a surplus in their social security but, is this going to continue? Think about it!

As you can see in this video, people is so used to spend their money buying a lot of things that they forget about what and how things will be in the future. I suggest this book in order to know more about the "consumerism": "The System of Objects, For a Critique of the Political Economy of the Sign, and The Consumer Society - Jean Baudrillard". The concept of sacrificing and building for a better tomorrow had been pushed a side by a live for today, easy credit and consumption order society. That's what I don't understand. People are thinking about just in themselves. Savings results in an increase in investment, additional research in development, a strong economy and a improve in the overall standard of living.

There are three types of people in this world: Those who save and invest, those who could easily save more but choose not to and those whom savings is very difficult. But who is the most injured when we talk about inflation? When the inflation rises people who are less well off will suffer more.

...

"So in that sense, if fiscal policy is lax or savings are exceptionally low, there is nothing monetary policy or any central bank can do about that. We cannot live in the present only, human beings cannot survive unless they create prevision for their future" - Alan Greenspan.

so...

Now I have one more question I would like to talk about. We already talked about public deficit, savings deficit and now I would like to talk about the trade deficit. What is this? "An economic measure of a negative balance of trade in which a country's imports exceeds its exports. A trade deficit represents an outflow of domestic currency to foreign markets." - Investopedia.

Take a look at the U.S trade deficit ticker here: http://www.americaneconomicalert.org/ticker_home.asp

In 2007, U.S was the last contry on a list of Trade Balance, it means the country had the worst trade deficit in 2007, but on the other hand China was the first at that list, according to the CIA World Fact Book.

If you are buying more than you selling, your trade partners are going to own a lot of your wealth. When a country has a low savings rates and the government has to borrow money to pay their bills, the trade deficit can be problematic.

|

China is the second larger holder of U.S treasuries and it is dangerous because it concentrate power in China's hand. If they would like to liquidate those treasuries, it would be a caos all over the world. Now take a look at the major foreign holders of U.S trasury securities here. So, are you still thinking that we just have to live the present? Aren't you been selfish? What about your kids? Think about it (again). |

Monday, November 1, 2010

Wednesday, October 27, 2010

The Best Motivation Video

Hello,

Today I saw a very nice video that inspired me a lot. For everybody like me that are in the beginning of professional life, this video shows that you can never give up.

Thursday, October 21, 2010

Foreign Inflows of Capital Tax in Brazil

An influx of dollar to Brazil has helped the real to appreciate by nearly 35% since the start of 2009. (Click here to see the USD/BRL 2Y chart). To control this inflow of dollar to the country, the government raised so- called IOF tax on foreigners’ investments in fixed-income securities to 6 percent from 4 percent. It also boosted the levy on money brought into the country to make margin deposits for futures market trades to 6 percent from 0.38 percent.

In fact, people believe that this tool will not work because this measure impact directly in the long-term yield increasing the spreads and the volatility between the internal and external prices to buy any type of asset in Brazil. Still, with the U.S. interest rates at low levels investors seek higher returns in emerging markets confirming the tendency to a strenghtening of the brazilian local currency.

Tuesday, October 19, 2010

Daily Readings Part 1

[...]Untermyer did not, apparently, think much of this answer, for he repeated his proposition: "Is not commercial credit based primarily upon money or property?"

Morgan: "No sir; the first thing is character."

Untermyer: "Before money or property?"

Morgan: "Before money or property or anything else. Money cannot buy it" - and he elaborated, after a few more questions - "because a man I do not trust could not get money from me on all the bonds in Christendom."[...]

This is an interesting part of the book I'm reading called Morgan - American Financier; by Jean Strause. I'm sure it is worth it.

Morgan: "No sir; the first thing is character."

Untermyer: "Before money or property?"

Morgan: "Before money or property or anything else. Money cannot buy it" - and he elaborated, after a few more questions - "because a man I do not trust could not get money from me on all the bonds in Christendom."[...]

This is an interesting part of the book I'm reading called Morgan - American Financier; by Jean Strause. I'm sure it is worth it.

Quem estrutura um IPO? Who is the IPO's architect?

Interessante,não? O que será que uma oferta inicial de ações (em inglês - IPO) tem a ver com um concerto musical? Se essa imagem está aqui é porque deve haver alguma ligação entre ambas.

Em um concerto musical, cada integrante da orquestra tem sua função previamente definida e compartilham o mesmo objetivo que é o de entregar ao ouvinte o que ele espera ouvir. O maestro, apesar de reger a orquestra sozinho, conta com o apoio do spalla (leader na Inglaterra, concertmaster nos EUA, konzertmeister em países de língua germânica) que, além de executar passagens solo, serve como regente substituto e repassa aos outros músicos as determinações do maestro.

Além dessa parte estrutural, podemos também citar o aspecto cultural da música erudita na orquestra. Ao contrário de outros gêneros musicais, a música erudita é dividida em andamentos e movimentos. O andamento se deve ao fato de que os compositores ao procurarem formas de indicar nas partituras a velocidade e expressão de suas músicas, não achavam soluções exatas - pela falta do metrônomo na época (séc. XVI), e assim colocavam nomes como largo (lento); adagio (calmamente); andante; moderato; allegro; vivace; presto(rápido), nomes típicamente italianos que foram adotados internacionalmente pela força de sua tradição musical. Dessa forma, cada parte das músicas, ou movimentos, leva consigo um nome que indica o andamento daquele trecho.

Quando uma empresa decide fazer uma oferta pública para vender valores mobiliários deve, obrigatoriamente, contratar um coordenador que, na analogia feita, possui as mesmas responsabilidades do que o maestro. O coordenador deve estruturar a operação de maneira que esteja tanto atraente para os investidores quanto para o emissor, ajudar a empresa a se transformar em sociedade por ações e obter o registro de cia. aberta - caso seja necessário, ajudar a empresa a preparar a documentação e ajudar a empresa a registrar a emissão pública na Comissão de Valores Mobiliários, formar o consórcio de distruibuição - caso seja necessário mais de uma instituição financeira para distribuir o volume de valores mobiliários, sendo colocado no mercado, realizar road-shows, ajudar na elaboração do prospecto, realizar o due-dilligence e distribuir os valores mobiliários juntos aos investidores.

Além do coordenador, há a presença do Agente Fiduciário (Pessoa Física ou Instituição Financeira) que é um ponto obrigatório em emissões públicas de debêntures. A principal função do agente fiduciário é representar a voz dos debenturistas perante a companhia em questão, realizando medidas para que os direitos desses investidores sejam resguardados.

Já o Banco Escriturador é o responsável pela escrituração e guarda dos livros de registro e transferência dos valores mobiliários escriturais. Detalhe, quando as ações e debêntures são emitidas de maneira escritural não existe cautela física, mas apenas o registro em contas de depósitos em nome dos titulares nos livros de registro do bando escriturador, tal registro caracteriza a titularidade da ação escritural ou da debênture escritural.

O banco Mandatário aparece nas emissões de debêntures e tem a missão de cuidar das movimentações financeiras, ou seja, recebe um nome do emissor os recursos que os investidores aportam na compra das debêntures e paga, por ordem do emissor, juros e amortizações referentes ao título. O Mandatário tem a função de permitir que o titular possa registrar sua debênture no Sistema Nacional de Debêntures, por isso o normal é que o banco escriturador acumule a função do banco mandatário.

Depois dos 3 atores, há a presença de um terceiro que é o custodiante. Podemos definir como uma instituição responsável pela guarda e manutenção das informações dos ativos componentes da carteira do investidor. É o custordiante que cuida para que o investidor não poerca seus direitos (dividendos, direitos de subscrição, etc).

Nas ofertas públicas é comum o ofertante contratar uma instituição financeira (corretora, distribuidora ou banco de investimento) para atuar no mercado com a intenção de estabilizar os preços dos valores mobiliários por um prazo determinado e por isso são chamados de formadores de mercados (market maker). Ele abre um preço de compra e outro de venda para os participantes do mercado secundário que queiram negociar os valores mobiliários, garantindo que os participantes do mercado tenham liquidez.

As agências de rating também são partes integrantes de uma oferta pública. Essas agências são empresas especializadas em levantar opiniões sobre o crédito das empresas por meio de notas (rating), as principais atuantes no Brasil são: Moody's, Standard & Poor's, Fitch Ratings, Atlantic Rating e Austin.

A junção destes 6 elementos (coordenador, agente fiduciário, banco escriturador, banco mandatário, market maker e agências de rating) fazem a oferta pública funcionar. Sem a presença de um deles isso não seria possível, seria dizer para uma orquestra executar um concerto para cello sem violoncelistas, não faria sentido. A procura do público por esta obra não será tão representativa quanto se houvesse total número de seus componentes para a realização de um evento. O mesmo ocorre com o IPO, se uma empresa emissora e as partes envolvidas não trabalham em harmonia ou se não há algum dos 6 elementos para atingir um resultado em comum, a qualidade da operação final não refletirá as expectativas do emissor.

Monday, October 18, 2010

Credit Default Swaps

Hello,

I told I'd be back on October 18. Today I was doing a research about what Credit Default Swaps is and how does it works. I found a lot of interest things like this video explaining about the CDS. Check it out.

Thursday, October 7, 2010

Holiday

Hello,

It's thursday night and I'm here relaxing listening to the bach cello's solo concert. By October 18 I think I'll be back to business. Meanwhile I will think about what I'm going to post on this blog. If you, viewer of this blog (I'm not sure if there is one soul in here), would like to ask about some issue, please feel free to comment!

Marcel Zanetti.

Junk Bonds

This week I was reading a story on The Economist about junk bonds. What are they? What are the advantages and disadvantages in buying them? Who uses junk bonds? I'll try to answer these questions in this post, I hope you enjoy it.

Junk Bonds are corporate debt securities, usually, with high credit risk, as indicated by Moody's (lower than Baa3) and Standard & Poor's (lower than BBB-). These kind of bond have a higher risk of default and in order to make it atractive to investors, it offers higher yields than better quality bonds.

Junk bonds offers companies several distinct advantages over other types of financing as equity dilution resulted from the issuance of new common shares. Bonds also can be less costly source of funds on after-tax basis than equity. On the other hand is the higher level of fixed charges that results from issuing bonds.The companies have to comply with the local comission (SEC for example) by giving a lot of information as financial reports, that companies may not wish to give for competitive reasons for example.

For the investor's viewpoint, these bonds can provide high income and a big potencial for capital gains. The word 'can' in the last phrase have a significance. The junk bonds is subject to a lot of high risks making the possibility of a default much higher than a investment-grade bond.

Besides, there are other people who use bonds. Funds are a great exemple of it. There are funds dadicated just to high-yield securities providing a diversification benefit. Other types of mutual funds also invest in high-yield bonds. Medium quality corporate bonds funds are typically permitted, by the provisions of their prospectuses, to allocate a portion of their assets to securities rated lower than Baa3/BBB-. This latitude enables the funds to raise the overall yield on their portfolios. Another category of high-yield investor includes "asset allocation funds," which achieve diversification by combining noninvestment-grade holdings with other fixed-income investments such as foreign bonds or mortgage-backed securities. Some equity mutual fund managers participate in the high-yield market as well. Their objectives include speculating in specific issues and increasing the income in their funds during periods in which the stock market offers little potential for capital gains.

Wednesday, September 29, 2010

Foreign direct investment (FDI) and the Latin America

According to a recently study developed by the United Nations Commission for America and The Caribbean (ECLAC), the most part of the investments in this region are directed to raw-material, services for the domestic market and low-tech industries. After two decades of the liberalization of the FDI, the productive structure still remain characterized by the low creation and diffusion of the knowledge.

But, the study also reported that there are countries that can extract benefits focused on the concept of the aggregated value such as Costa Rica that attracted just US$ 1.32 billion (US$ 343 million in manufacturing industry and US$ 893 million in the services sector) in the last year but directed it to the investments on high-tech industries such as Boston Scientific, Allergan and Hollorgic.

On the other side, there are countries as Brazil that will remain labeled as commodity exporter unless the Central Bank intervene to avoid an excessive Real appreciation followed up by a decreasing interesting rate (The interest rate benchmark is currently at 10.75 percent). The second step it would be a wide change in the national monetary policy to improve the systemic competitiveness of the country (Brazil's corporate Tax for 2010 is 34%) and stimulate the industrial policies that generates a increase in the economic value of the country exports.

Global companies are shifting technological jobs to less developed contries so these countries need to setup strategies to be prepared to meet demand and be able to boost their economy creating more value, improving the educational system and the population's condition.

Sunday, September 26, 2010

Next step

Today this blog is heading for a big change. I will try to reach every country through the use of the english as official language.

The main purpose is to create a networking related to people who are interested to discuss about business and finance. To succeed, I'll approach the local issues through a global view allowing people to expose their point-of-view.

I hope that this idea can work out.

Graciously,

Marcel Zanetti.

Wednesday, September 22, 2010

Entenda a Previdência Privada

Em suma, podemos dizer que Previdência Privada é um sistema onde seu dinheiro é acumulado, garantindo uma renda mensal no futuro, especialmente quando deseja parar de trabalhar.

Em linhas técnicas, é uma forma de seguro contratado para garantir uma renda futura ao comprador deste seguro ou ao seu beneficiário. O prêmio (renda) é calculado conforme a entidade gestora onde o cliente decidiu realizar este tipo de seguro. Existem no Brasil, dois tipos de plano de previdência, são eles: o aberto e fechado.

Aberta - Aquela que é oferecida por seguradoras e bancos, assim, podendo ser contratada por qualquer pessoa;

Fechada - Direcionada para funcionários de empresas, sindicatos ou sociedades de classes. Neste caso, o empregado banca com uma parte mensal do salário e a empresa se compromete a bancar o restante. Há a existência de casos em que a empresa paga não só uma parte mas como toda contribuição destinada à previdência.

Thursday, September 16, 2010

O que significa a intervenção do BoJ no câmbio

O efeito taxa de câmbio, mecanismo integrante da política monetária, é uma importante ferramenta que influencia a demanda agregada. Através da taxa de câmbio, é possível aumentar a exportação e, por consequência, aquecer a economia.

Quando se tem uma taxa de câmbio valorizada, isto é, quando a moeda local está muito valorizada em relação a outras moedas, há a ocorrência de menos exportação, o que desaquece a economia do país.

O Japão atualmente exporta equipamentos de transporte, veículos motorizados, produtos eletroeletrônicos, máquinas industriais, ou seja, produtos manufaturados.Os principais compradores destas exportações são os EUA, China e Coreia do Sul. No mercado internacional, as mercadorias são negociadas, principalmente, em dólar, o que explica o movimento de intervenção do Banco do Japão no mercado cambial nesta quarta-feira.(Não sabe do que se trata? Clique aqui.)

O país, com a economia se recuperando, é imprescindível que tenha um iene mais fraco para tornar as exportações japonesas mais baratas e aumentar o lucro dessas empresas, aliviando a pressão sobre uma economia frágil.

Wednesday, September 8, 2010

Capitalização da Petrobrás - Geração de Valor

Na semana passada houve uma forte discussão em relação a capitalização da Petrobrás que acontecerá este ano. De acordo com os 5 bilhões de cessão onerosa da União cedida à Petrobrás, Guido Mantega afirmou que a TIR(Taxa Interna de Retorno) será de 8.83% a.a, uma vez que o valor médio do barril foi definido em US$ 8,51.

O que isto quer dizer:

Em teoria, a taxa interna de retorno é a taxa de desconto que faz com que o valor presente do projeto seja zero, isto é, esta é a taxa que remunera o investidor. Se o valor presente do projeto fosse negativo, significa que ele teria que desembolsar mais e assim tornando o investimento inviável.

No caso da Petrobrás, a TIR deste projeto é praticamente igual ao custo de capital(mix de dívida + capital próprio) que a empresa possui. Como ela apresenta um grande endividamento (atualmente em 34% e com o teto de 35%) fez-se o uso da capitalização, isto é, um aporte de capital através da emissão de novas ações.

Qual o impacto para os acionistas?

A curto prazo pode-se dizer que os acionistas não se beneficiarão com a capitalização, uma vez que a TIR do projeto é quase igual ao custo de capital. Para a geração de valor imediato para o acionista, a TIR deveria ser bem maior que o custo de capital. Entretanto, a capitalização possibilitará que a empresa explore o pré-sal e com isso aumente seu lucro e, portanto, o valor para o acionista.

Monday, August 30, 2010

American Depositary Receipts (ADR)

Antes de chegar diretamente ao ponto das ADR's é preciso fazer uma pequena explicação sobre o que são os DR's(Depositary Receipts). DR's são títulos negociados em um país que tem como lastro, ações de uma empresa que está instalada fora deste país, um bom exemplo disso são as ADR's da Petrobrás que são negociadas na Bolsa de Nova Iorque.

Os ADR's são divididos em 3 tipos:

Programa nível I: Envolve o lançamento de certificados no mercado norte-americano para negociação apenas em balcão, isto é, fora da bolsa. A vantagem deste nível é que as empresas não precisam se adequar as normas contábeis dos Estados Unidos (US GAAP, IFRS...etc) e que a empresa tem a possibilidade de tornar seus papéis conhecidos no exterior. Estas ações estarão guardadas no banco custodiante e a emissão dos ADR's é feita pelo banco depositário no exterior. Uma informação importante é de que as ações negociadas neste nível são lastreadas em ações negociadas no mercado secundário do país onde a empresa tem sede, isto é, não há emissão de novas ações para posterior negociação da bolsa americana.

Programa nível II: Aqui, embora os recibos não representam novas ações, a empresa deve atender as normas contábeis norte-americanas, assim como a um maior número de exigências da SEC.

Programa nível III: Neste caso há emissão primária de papéis que serão negociados na Bolsa de Valores ou no Nasdaq. Aqui há uma captação efetiva de novos recursos. Neste nível a empresa deve atender todas as exigências da SEC,das normas da bolsa americana e também da contabilidade americana.

Arbitragem entre ADRs e ações no Brasil:

A arbitragem é qualquer operação que permita gerar valor sem risco de mercado, ou seja, sem o risco da desvalorização ou valorização dos ativos, assim, como as ações são negociadas em mercados distintos, compra-se o ativo no mercado onde o preço é menor e vende-se no mercado onde o preço é maior, entretanto vale ressaltar que esta operação tem custos, neste caso, custos no mercado local e quanto nos EUA.

Monday, August 23, 2010

Aumento da taxação sobre o capital nos EUA Jan/2011

Imagem do Wikipedia.

Em 2001 e 2003, o congresso do GOP(Grand Old Party) promulgou diversos cortes de taxas para investidores, donos de pequenos negócios e famílias. Estes benefícios serão expirados em Janeiro de 2011(Você pode olhar o arquivo completo no site do Comitê de Taxação, clique aqui).

Agora, o que isso tem a ver?

Pelos percentuais, parece que este será o maior aumento de taxas já visto nos EUA. Todas as faixas do imposto de renda serão aumentadas, sendo que os mais pobres sofrerão a maior taxação, segue abaixo a tabela com os valores:

1ª Faixa: De 35% para 39,6%

2ª Faixa: De 33% para 36%

3ª Faixa: De 28% para 31%

4ª Faixa: De 25% para 28%

5ª Faixa: De 10% para 15%.

Com este aumento, alguns jornalistas dizem que pode afetar diretamente a economia americana, uma vez que as pessoas terão menos dinheiro para gastar, mas Obama diz ser necessário este aumento pois a divida americana em 2010 deve subir para $13,7 trilhões ou 65% do PIB.

Thursday, August 19, 2010

Commodities

No começo de 2008 até Julho de 2010, investidores colocaram, aproximadamente, 61 bilhões de dólares em fundos mútuos e ETF's ligados a commodities. Durante o mesmo período, fundos e ETF's com origem nos EUA sofreram saída de dinheiro na ordem de, aproximadamente, 53 bilhões de dólares, segundo o site MorningStar.

Já em 2010, fundos mútuos relacionados à commodities atraíram mais de $ 12 bilhões.

O que representa esse movimento para fundos como estes e, também, instrumentos de renda fixa(títulos públicos)?

Tal acontecimento se deve ao fato do maior aversão ao risco por parte do investidor. Para se proteger do mercado turbulento, investidores apostam na diversificação dos seus investimentos em fundos como o de commodities e títulos públicos, no qual proporciona um retorno seguro para quem aplica.

Por consequência dessa migração para commodities e títulos, há quem diga que a próxima bolha será relacionada aos títulos públicos como o jornalista David Callaway em sua matéria "Big investors pulling the exit chute" para o site MarketWatch. Entretanto há quem discorde, como o jornalista da agência Reuters, Felix Salmon, em sua matéria "The Treasury-bubble meme". Bom, como dizia Benjamin Graham "Faça sempre sua análise e seu julgamento pois o dinheiro é seu".

Monday, August 16, 2010

O caso de deflação no Japão

(Clique na figura para ampliar)

No segundo trimestre deste ano a economia do Japão apresentou um crescimento de apenas 0,4%. Isto se deve ao fato de, principalmente, ter uma grande expectativa na estagnação do consumo e da exportação, uma vez que a moeda local(Japanese Yen) está muito valorizada(USDxJPY) e por causa da deflação que persegue o país desde o início da década de 90.

No começo da década de 90, o governo japonês tentou eliminar a deflação a partir da redução da taxa de juros para zero que, na teoria, faria com que o consumo e a produção de bens aumentassem e, consequentemente aquecesse a economia. Entretanto, essa política não surtiu o efeito desejado.

Uma baixa taxa de desemprego e um baixo crescimento do PIB são os principais fatores que perpetuam a deflação no Japão. Se a taxa de crescimento do PIB cresce pouco, como agora neste segundo trimestre, a taxa de desemprego deveria aumentar, o que implicaria em uma menor renda familiar, porém não é o que acontece na realidade. O país mantém uma taxa de desemprego baixa comparada a outros países, isto é, os japoneses são mantidos no trabalho, porém ganhando menos, o que implica em menos consumo interno, o que gera a deflação.

(Clique na figura para ampliar)

Wednesday, August 11, 2010

A taxa referencial no seu dia a dia

A taxa Referencial(TR) teve origem no Plano Collor II para ser o principal índice brasileiro - uma taxa básica referencial de juros a serem praticadas no mês vigente e que não refletissem a inflação do mês anterior, segundo o PortalBrasil. É calculada com base em uma cesta formada por CDBs dos 30 maiores bancos do país.

Esta taxa corrige os saldos mensais das cadernetas de poupança que neste ano apresenta um acumulado de 4.49%. Pelas regras vigentes, as cadernetas de poupança são remuneradas pela TR mais um percentual de 0.5% ao mês.

Além da caderneta de poupança, a taxa referencial funciona como benchmark para diversos instrumentos financeiros como o Fundo de Garantia por Tempo de Serviço(FGTS) que é corrigido pela TR + 3% ao ano ou então, o financiamento imobiliário pelo Sistema Financeiro de Habitação.

Em 2010 percebe-se que a TR mensal andou sempre próxima a 0, só não ficou negativa por consequência de uma resolução do Banco Central que impede que a TR tenha um valor negativo. A explicação para estar sempre próxima a 0 se deve pelo fato de que o Brasil, tornando-se uma economia mais saudável e estável, as taxas de juros serão mais baixas, tanto para quem toma empréstimo quanto para quem investe. Assim, é natural que os percentuais sejam menores, agora que o país livrou-se do seu passado de hiperinflação, calote da dívida pública e congelamento dos preços.

Saturday, August 7, 2010

Por que os ETF's?

Em Janeiro de 1993, foi criado o primeiro Exchange Traded Fund(ETF) que representava o índice S&P 500. Na Bolsa de Valores Americana(NYSE) a ação deste fundo, que é negociado pelo símbolo SPDR, representa aproximadamente um décimo do valor do S&P 500.

ETF's são como ações negociáveis em Bolsa de Valores e que tem por objetivo representar um determinado índice de ações ou títulos. Investidores poder fazer qualquer coisa com um ETF como fazem com ações por exemplo, venda a descoberto. Por serem negociados na bolsa de valores, eles podem ser comprados e vendidos a qualquer hora do dia ao contrário de fundos mútuos.

Comparado com fundos mútuos, os ETF's têm menor custo porque enquanto os fundos mútuos cobram uma taxa de administração entre 1 e 4%, ou mais, você gastará entre 0.1% a 1% dependendo das taxas cobradas pela sua corretora.

Além disso, por ser negociável em bolsa de valores, o investidor não necessita abrir mão de muito capital como é necessário fazer em alguns fundos mútuos. Os investidores podem traçar diversas estratégias como vender a descoberto ou colocar um stop-loss, algo também não possível nos fundos mútuos, que por sua vez, trabalham com a estratégia da valorização e pagamento de dividendos do seu portfólio.

Saiba mais em:

Wednesday, August 4, 2010

O investidor e as flutuações de mercado

{kind=link}

Olá,

Há um tempo atrás li um livro chamado "The Intelligent Investor" de Benjamin Graham que, para mim, todos que apresentam alguma relação com finanças deveriam ler. Para estimulá-los um pouco mais a leitura, Benjamin foi amigo e mentor de Warren Buffet, tanto que tem um prefácio escrito pelo próprio Buffet neste livro. Fica a indicação.

Como usual, costumo fazer anotações em um caderno dedicado a finanças e hoje estava revisando algumas coisas e decidi postar algo bastante interessante que anotei a partir deste livro.

O Investidor e as flutuações de mercado

Tudo é questão de disciplina. O mercado ao longo do tempo fará com que seu portfólio sofra oscilações grandes, tanto positivamente quanto negativamente.

Apesar das flutuações, é necessário manter a disciplina e concordar com os objetivos iniciais que coordena seu portfólio.

Em meados dos anos 90, as previsões de estrategistas de mercado se tornaram mais influentes do que nunca. Eles não, infelizmente, se tornaram mais precisos.

Em 10 de Março de 2000*, o dia em que o Indice NASDAQ atingiu sua máxima história de 5048.62 (nº 1 no char abaixo), um chefe analista de uma empresa de serviços financeiros disse a um jornal que ele esperava que o NASDAQ atingisse 6000 pontos dentro de 12 a 18 meses. Cinco semanas depois, o índice já havia caído para 3321.29 pontos(nº2 no chart) - mas um estrategista de mercado de uma outra companhia declarou que havia mais 200 ou 300 pontos de queda para que o índice subisse novamente. Em seguida verificou que não havia tido altas, mas apenas quedas, até que o índice NASDAQ atingiu seu mínimo histórico de 1114.11(nº3 no chart) em 9 de Outubro de 2002.

Em Março de 2001, um chefe de estratégia de investimento de um renomado grupo financeiro, preveu que o índice S&P500, que reune as 500 empresas mais representativas do país, fecharia o ano de 2001 em 1650 pontos e que o Dow Jones chegaria ao final de 2001 a 13000 pontos. "Nós não esperamos recessão", disse o chefe de investimento, "e nós acreditamos que os lucros da empresa vão crescer a altas taxas este ano". A economia dos EUA estava entrando em recessão como ela havia dito, e o S&P500(nº 4 do chart) fechou o ano de 2001 em 1148.08, enquanto o Dow Jones terminou em 10.021,50(nº 5 do chart) - 30% e 23% abaixo das previsões do chefe de investimento, respectivamente.

(Trecho retirado do Livro "The Intelligent Investor" pag.190. - Edição Revisada).

O chart fica muito grande na página, então fiz o upload, o link está abaixo:

Legenda:

GSPC - Standard & Poor's 500

IXIC - NASDAQ

DJI - Dow Jones

Se a razão pela qual a pessoa investe é a de ganhar dinheiro, então seguir conselhos é pedir aos outros falarem como ganhar dinheiro. Por isso devemos sempre ter cuidado ao que escutamos, seja do analista da sua corretora ou de um jornal renomado, pois cada instituição ou pessoa quer defender seus próprios interesses(buy side e sell side). Sempre devemos fazer nossa própria análise, desenvolver nosso feeling para que ter uma visão crítica do que está ao nosso redor.

Subscribe to:

Posts (Atom)